After-hours trading on the rise; small- and mid-cap stocks lead the charge, ETFs losing share

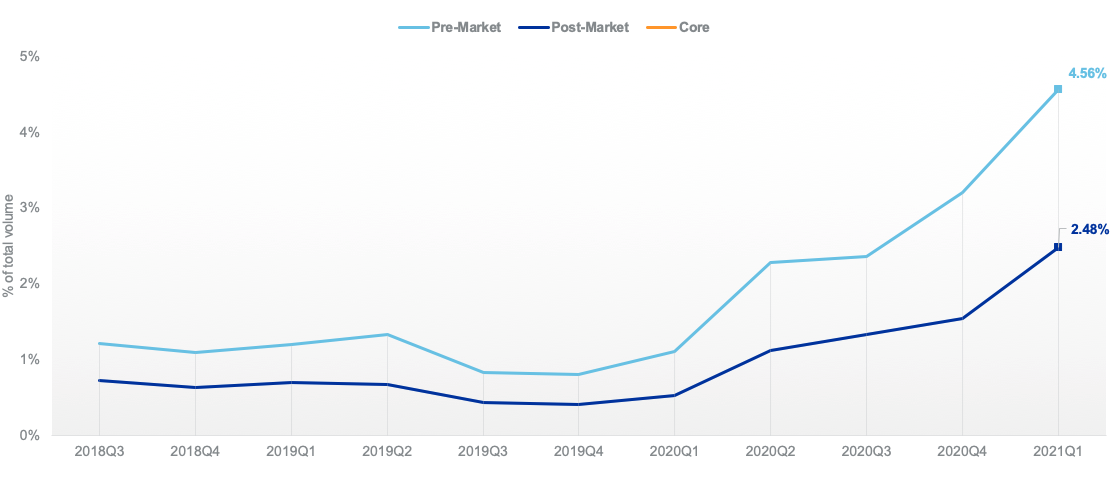

As evidenced in Figure 1 below, after-hours trading volumes for single-name stocks have been increasing at extraordinary rates since Q3 2019. Pre-market volumes were 4.56% of trading volume in Q1 2021 vs 0.83% in Q3 2019, and post-market volumes also jumped to 2.48% vs 0.43% for Q3 2019.

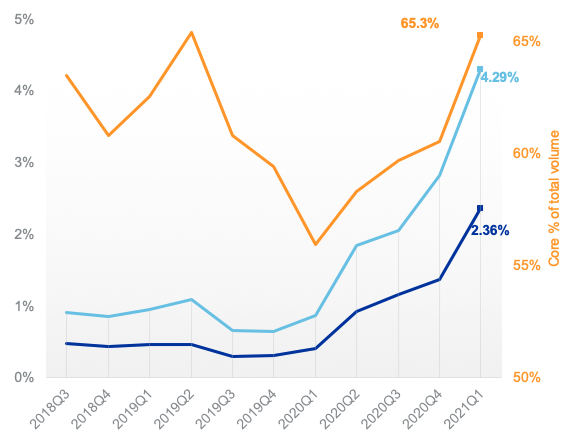

The primary driver of this growth is not large-cap S&P 500 names, but rather small- and mid-cap names. As seen in Figure 1, pre-market volumes for non-S&P 500 names have jumped from a mere 0.65% of the total stock volume in Q3 2019 to a staggering 4.29% within five quarters. Similarly, the post-market volume share for these names has grown almost eight-fold, from 0.30% to 2.36%.

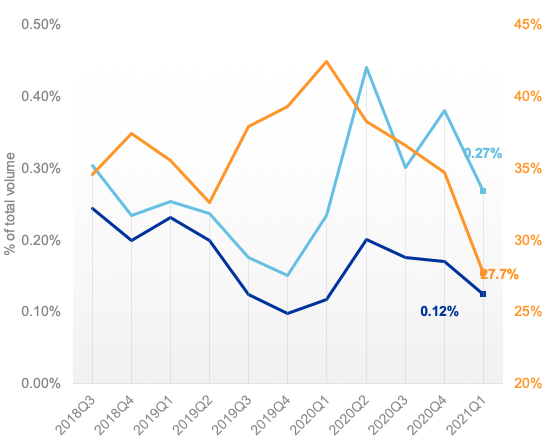

In very sharp contrast, pre-market volumes for S&P 500 names have increased from 0.18% to 0.27% of market volume within the same time frame, with the equivalent post-market numbers struggling to stay constant at 0.12%. The trend is similar in the core trading session, with non-S&P 500 stocks capturing an increasing share of the total volume.

Figure 1

Session Volume as % of Total Single Stock Trading Volume

S&P 500 Volumes as % of Total Trading Volume

Non-S&P 500 Volumes as % of Total Trading Volume

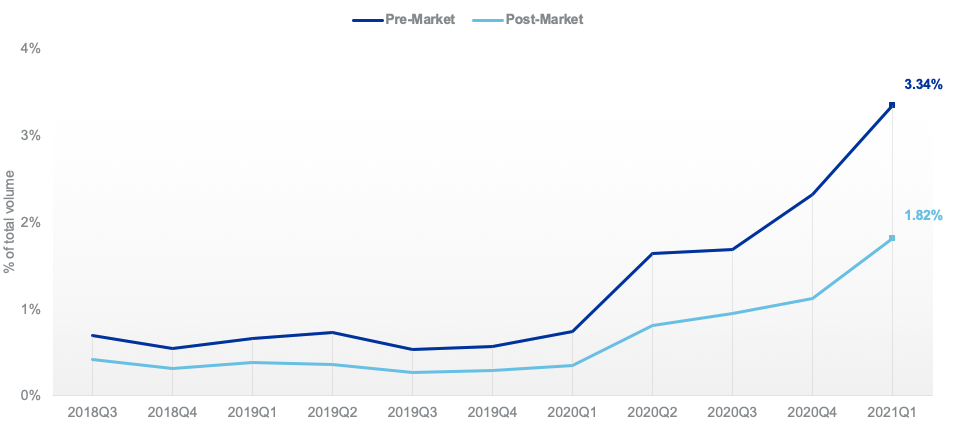

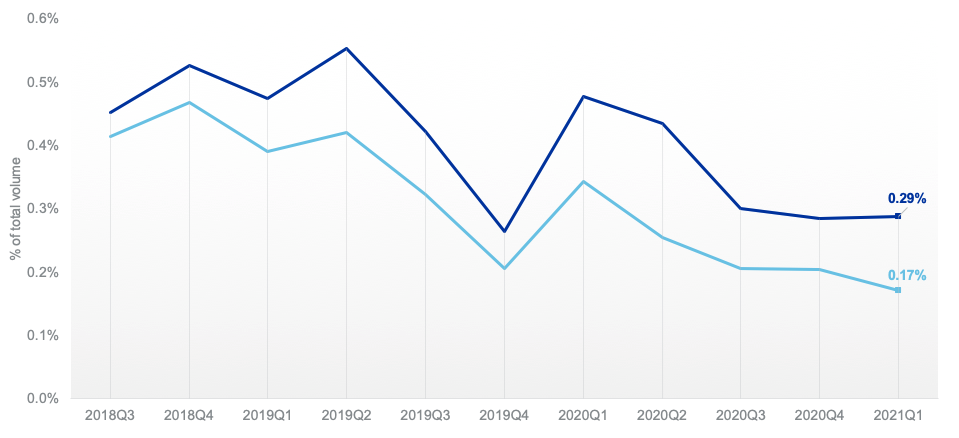

Figure 2 shows that single stocks have fueled the after-hours volume growth, with pre- and post-market volume increasing from sub-1% of the total market in Q3 2019 to 3.34% and 1.82% respectively by Q1 2021.

ETFs, on the other hand, have seen their after-hours share of total volume decrease during the same period - the pre-market share has fallen to 0.29% of the total volume in Q1 2021 (vs 0.42% in Q3 2019), while the post-market equivalent has also dropped to 0.17% (vs 0.32% in Q3 2019).

Figure 2

Single Stock Volume as % of Total Trading Volume

ETF Volume as % of Total Trading Volume

Earnings announcements less of a catalyst but retail-sized participation growing

Earnings announcements are a traditional driver of after-hours trading activity, but have displayed much less influence in the last year while retail-sized volumes are increasing their share of the earnings volume pie.

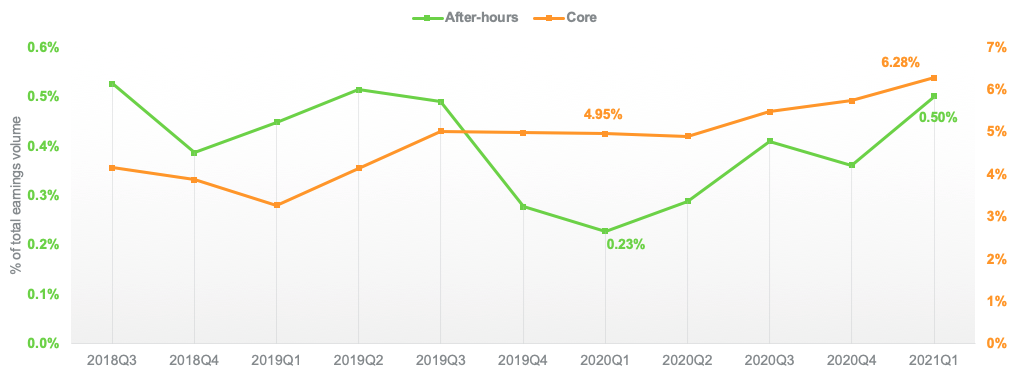

Retail-sized volumes have grown to account for 0.50% of after-hours earnings volumes1, up more than 100% since Q1 2020. This follows the trend in the core trading session, where retail-sized volumes represent 6.28% of core-trading earnings volumes (vs 4.95% in Q1 2020).

Figure 3 also shows the share of S&P 500 session volume from earnings events (including a projection for total Q1 2021). Both sessions have increased earnings-related volumes since Q3 2018, but the share of total volume related to earnings has fallen sharply during the pandemic. This suggests that macroeconomic factors and non-earnings news have been more impactful to stock liquidity, with after-hours retail-sized flow interactions becoming more likely.

Figure 3

Retail-sized Volume as % of Total Earnings Volume

Earnings Volume as % of Total S&P 500 Session Volume

* Data for 2021 Q2 is projected using data up to 05/20/2021, assuming quarter averages persist.

After-hours retail-sized presence growing

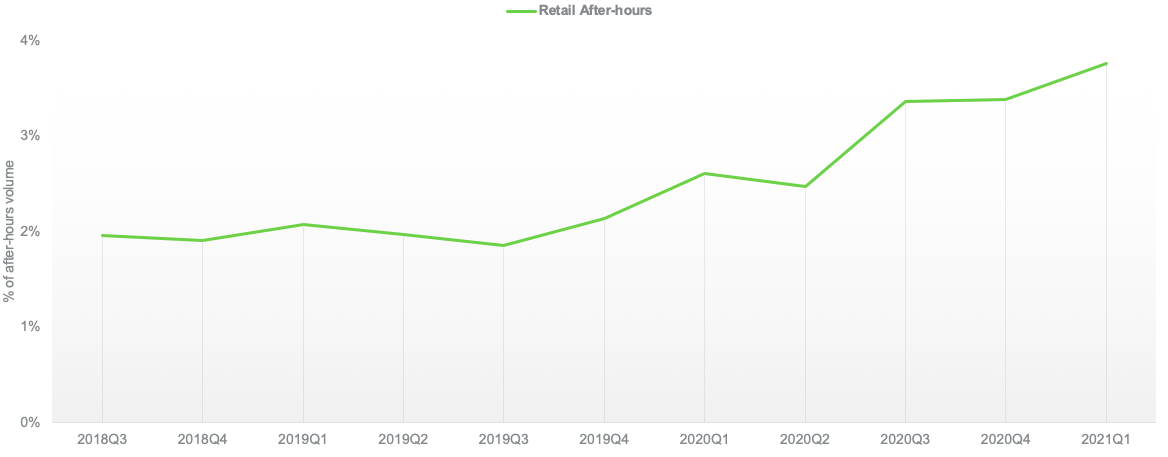

The pandemic- and lockdown-induced boost in retail-sized trading activity which emerged during the spring of 2020 has impacted after-hours trading as well.

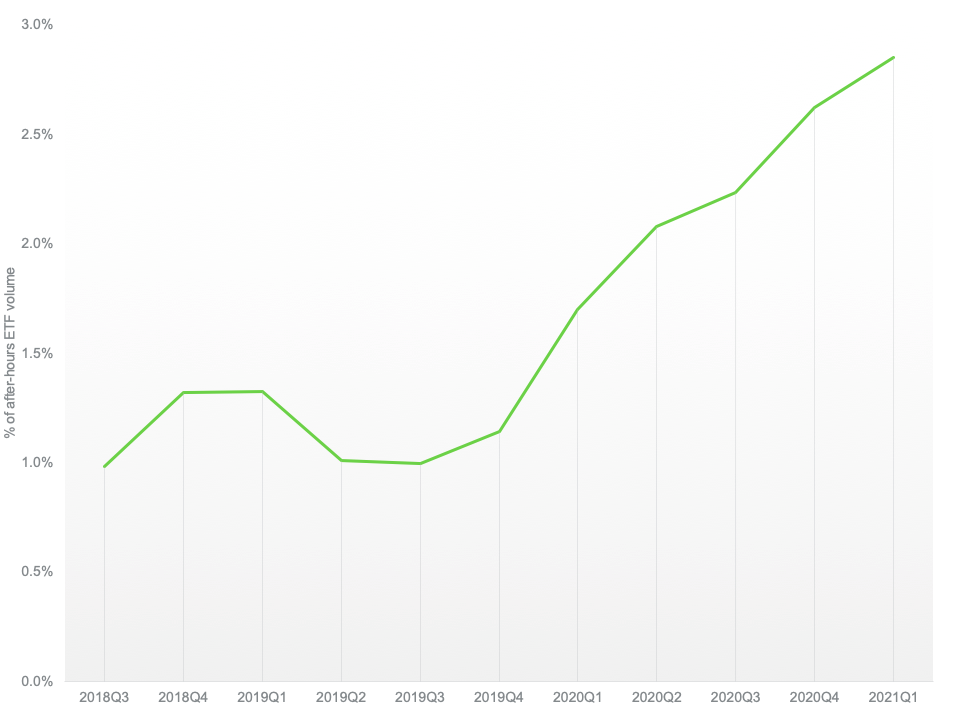

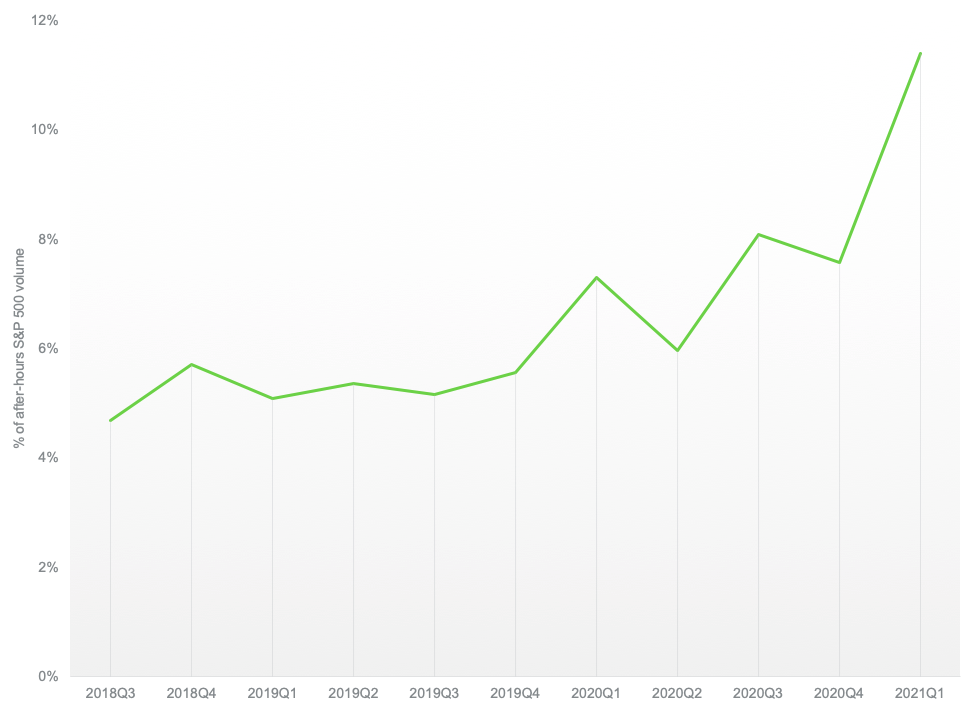

Figure 4 shows the retail-sized share2 of after-hours trading increased substantially since Q4 2019. Retail-sized activity now accounts for 3.75% of the after-hours sessions, up from the pre-pandemic value of 2.14% for Q4 2019.

This retail effect is more pronounced when we look at the retail-sized share of ETF and S&P 500 volumes separately. In each case, retail-sized activity has more than doubled; retail-sized volume now represents 2.85% of after-hours ETF volume (vs 1.14% in Q4 2019) and 11.40% of after-hours S&P 500 volume (vs 5.56% in Q4 2019), further illustrating the shifting dynamics from increased retail participation.

Figure 4

Retail-sized Volume as % of After-hours Volume

Retail-sized Volume as % of Session ETF Volume

Retail-sized Volume as % of Session S&P 500 Volume

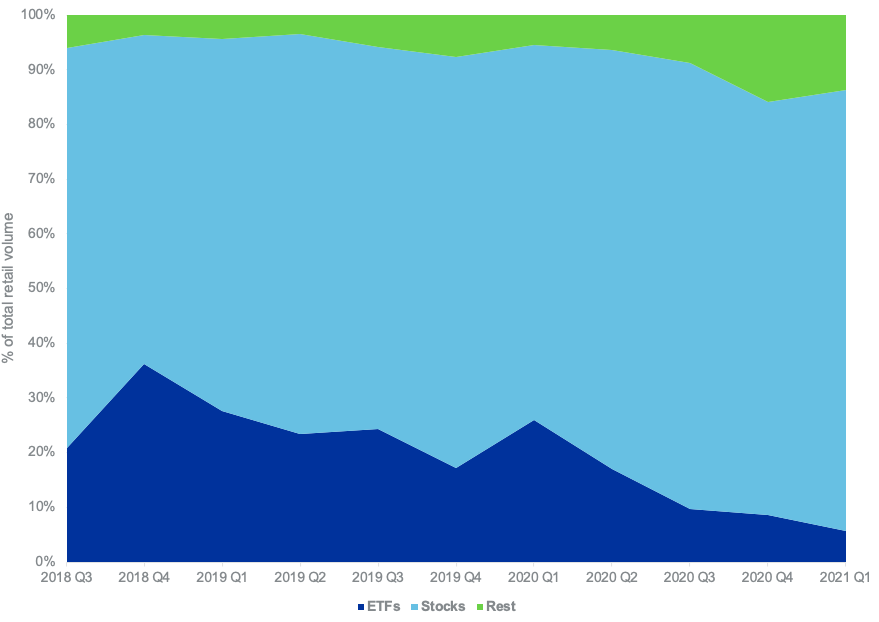

Despite this common retail trend across stocks and ETFs, retail activity still seems to favor stocks over ETFs as a trading instrument. The ETF share of that volume has dropped from 17% in Q4 2019 to just over 5% in Q1 2021, while the stock share has seen an increase from 75% to 81%.

Figure 5

Instrument Volume as % of Retail-sized Volume

NYSE Arca gains ground

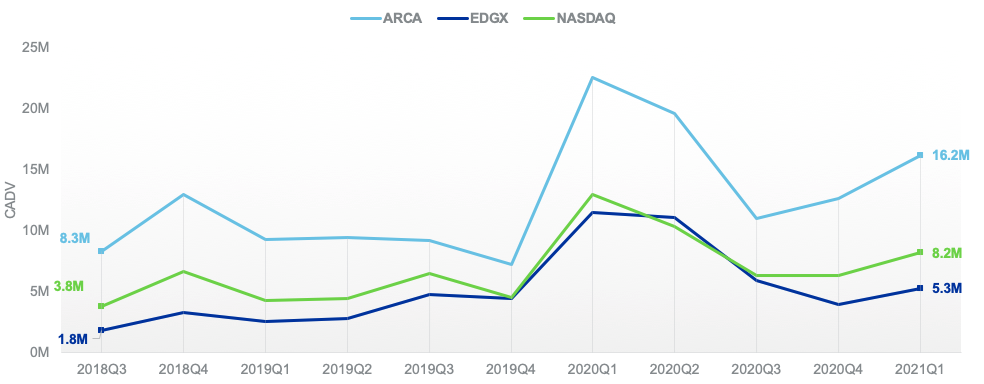

Higher market volatility and increased retail activity has led to a higher share of after-hours trading taking place on NYSE Arca.

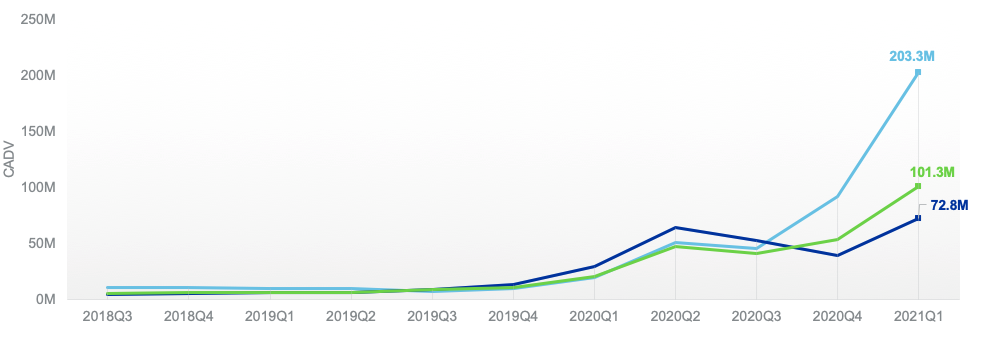

As evidenced in Figure 6, Arca ETF volumes are back on an upward trend heading towards the highs of 2020 Q1 and steadily widening the gap from the other exchanges. Stock volumes have reached multi-year highs during the previous two quarters, with NYSE Arca benefiting the most and widening the gap from the rest of the market.

Figure 6

After-hours ETF Volume by Exchange

After-hours Single-name Stock Volume by Exchange

Conclusion

The less-researched and less-documented space of after-hours trading has seen shifting dynamics since the onset of the pandemic. After-hours trading volumes are on the rise, due to growth in small- and mid-cap stocks more than large-cap or ETFs. Earnings announcements have displayed less influence on after-hours trading, with retail traders capturing an increasing piece of the earnings-related volume while their presence in after-hours trading continues to climb.

Our next post on this topic will examine how these changes influence price discovery in the after-hours market and into the Opening Auction.

NYSE Research Insights

Find all of NYSE Research's articles on market quality, market structure, auctions, and options.