Behind the Record Volumes: A Hidden Opportunity

By: Stefanos Bazinas | Head of Research & Analytics, NYSE

April 8, 2026

The NYSE Closing Auction has long been the largest single liquidity event in US equities trading and, lately, every calendar quarter has brought new volume records. The first quarter of 2026 was no exception, as the NYSE traded a record 605.5mn shares (accounting for over $43bn) daily at the closing auction. Individual daily records were also crushed – a new record 3.57bn shares were matched at the NYSE Closing Auction on March 20th, 2026 for a record total of $230.5bn.

As the closing auction continues to grow, maximizing participation opportunities and minimizing price impact become ever more important for market participants. Below we provide – for the first time ever – an inside view into residual interest that does not get filled during the NYSE Closing Auction.

Quantifying Untapped Auction Liquidity

As shown in Figure 1, in 2026 Q1, a total of 18mn shares remained unfilled on a daily basis due to a lack of contra-side liquidity even though they were eligible to participate at the closing auction price. Almost two thirds of these unexecuted shares came from small- and mid-cap symbol auctions where opportunities remain ripe for market participants. This untapped liquidity accounts for over $530mn daily, reaching close to $1bn on major rebalance days (MSCI, Russell, S&P).

Figure 1

Since the start of 2025 – and as the size of the NYSE Closing Auction has increased dramatically – market participants have taken advantage of these opportunities to interact with available liquidity at a very fast pace. Even so, this untapped liquidity still accounts for roughly 3.3% (Figure 2) of the total closing auction executed volume despite its downward trend. This figure jumps to over 6.3% of auction volume when narrowing in on symbols that are not constituents of the Russell 1000 (i.e. small- and mid-cap stocks).

Figure 2

Figure 3 shows the percentage of unique NYSE Closing Auctions that see at least 1-15% of their executed volume cancelled back to market participants because of the lack of opposite-sided interest. More than one out of every four (or one out of every three for small- and mid-cap stocks) NYSE Closing Auctions have at least 2% of their executed volume cancelled back to market participants, despite these shares being marketable at the closing price. More than one out of every seven NYSE Closing Auctions have at least 5% untapped, while more than 5% of auctions have an extra 10% or more shares available to trade at the closing price.

Figure 3

The Relationship between Auction Size and Residual

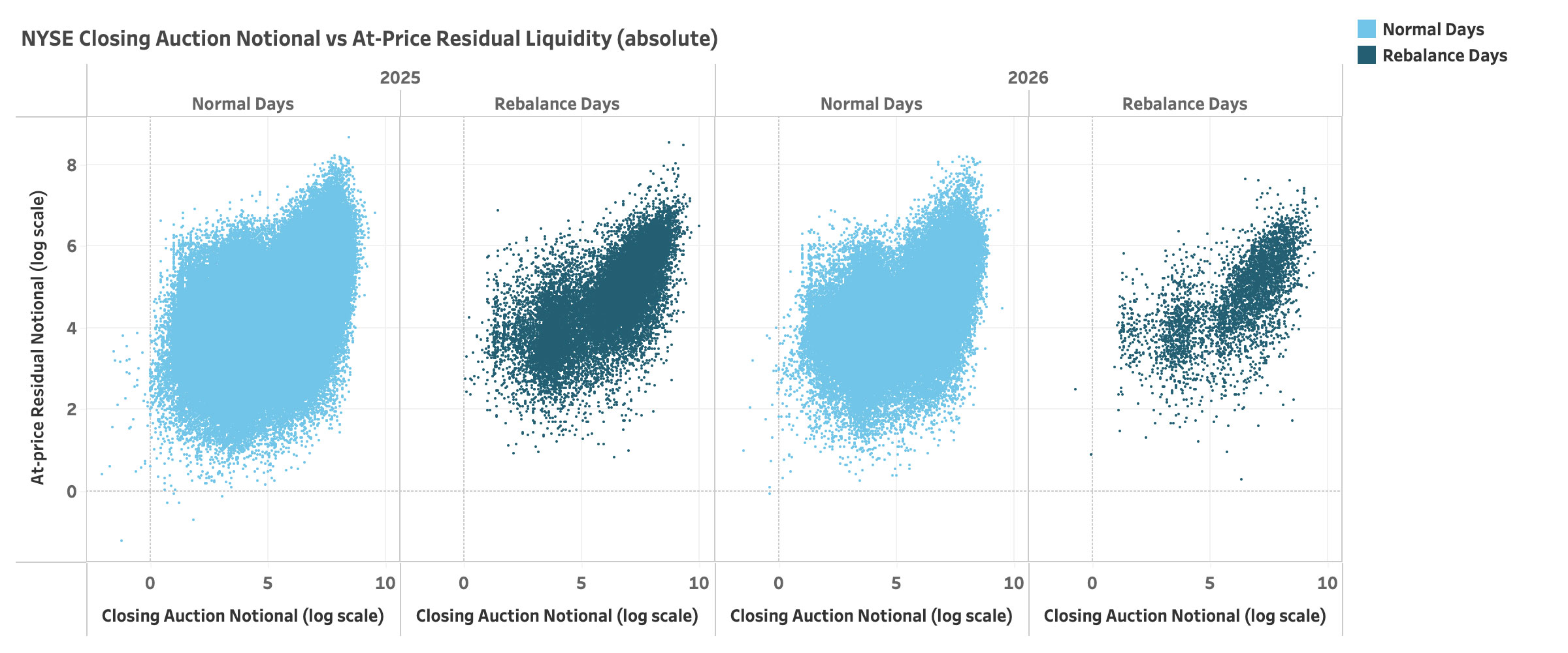

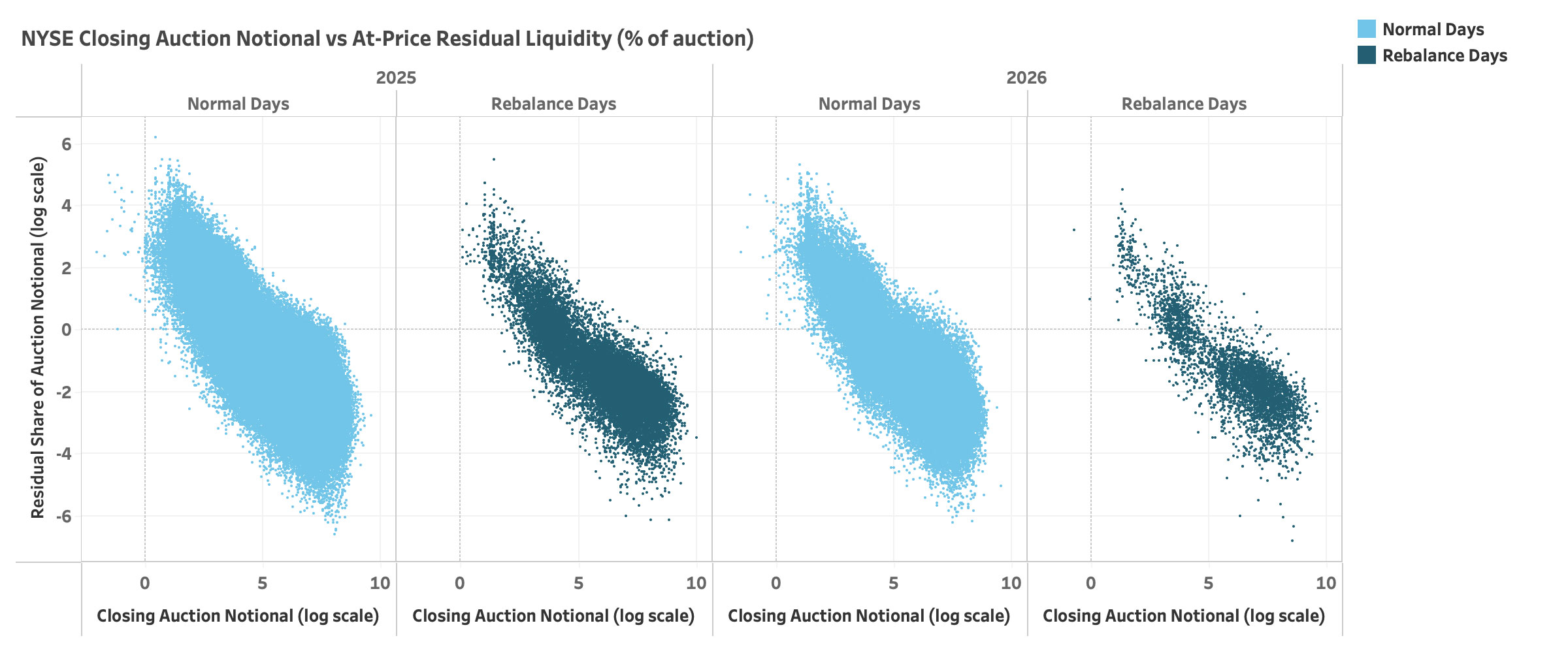

Figures 4a-b show two scatter plots depicting all NYSE Closing Auctions since the start of 2025. Figure 4a shows closing auction executed notional plotted against closing auction residual notional for each auction (both in log scale), showing a positive relationship between the two – albeit noticeably stronger on rebalance days. In other words, larger NYSE auctions tend to have more unexecuted notional at the closing price. This difference makes sense intuitively, as higher participation increases the chances of more liquidity being available to trade (and also not trade) at different prices. Figure 4b shows the same closing auction executed notional now plotted against closing auction residual notional expressed as a share of the former (still in log scale). Here the trend reverses sharply and becomes clearly negative. What does this mean? In simple terms, the first figure shows that bigger auctions tend to yield larger residual size, and the second figure shows that bigger auctions are proportionally better at filling this residual interest.

Figure 4a

Figure 4b

A Closing (Offset) Opportunity

The above analysis showcases the consistent prevalence of large liquidity opportunities in the NYSE Closing Auction, even as it continues to reach new records every quarter. The NYSE Closing Offset (CO) order type allows market participants to directly interact with this liquidity while at the same time minimizing the potential price impact of these orders.

Have a question?

Reach out to your NYSE Relationship Manager with any questions or to learn more about Closing Offset orders.

Related resources

- See moreNYSE Research Insights

- View moreNYSE Pillar®

Our integrated trading technology platform, stress test proven with the lowest latency out there

- View moreHistorical Data

Purchase or trial subsets of NYSE Historical TAQ Data available from 1993 - present

- View moreICE Vox

See news and insights from across ICE