April 8, 2020

“Unprecedented” is an apt descriptor for our Options business in the first quarter. The period continued a record-breaking volume trend over the last two years, and here we review factors that defined the magnitude of Q1.

Volume

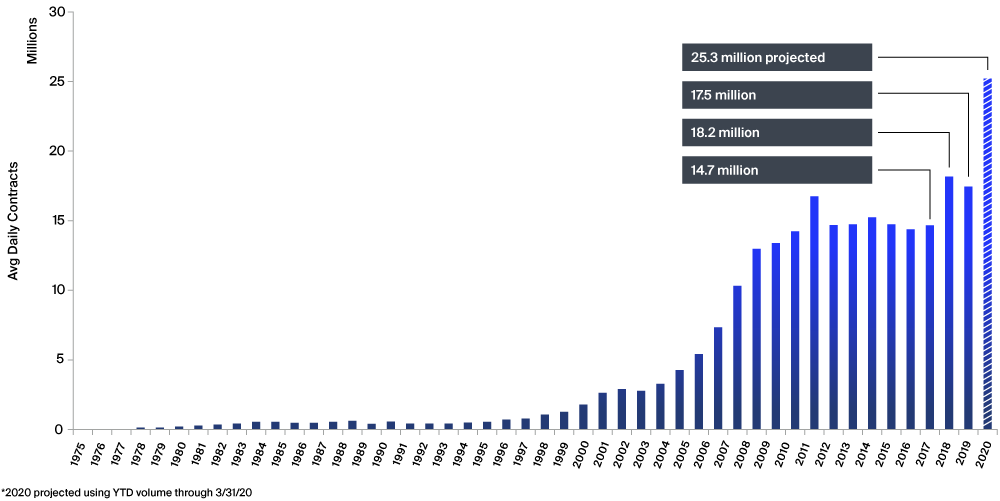

Over the last two years the options industry has experienced its highest recorded volume. This growth continued and accelerated in 2020, with record volume set in January despite a muted volatility environment. As volatility returned in late February and March, fresh records were set, including the two most active days for multiply-listed options with 40.3 million contracts traded on February 27 and 42.8 million contracts traded on February 28.

Equity and ETF Options ADV

Floor Closures

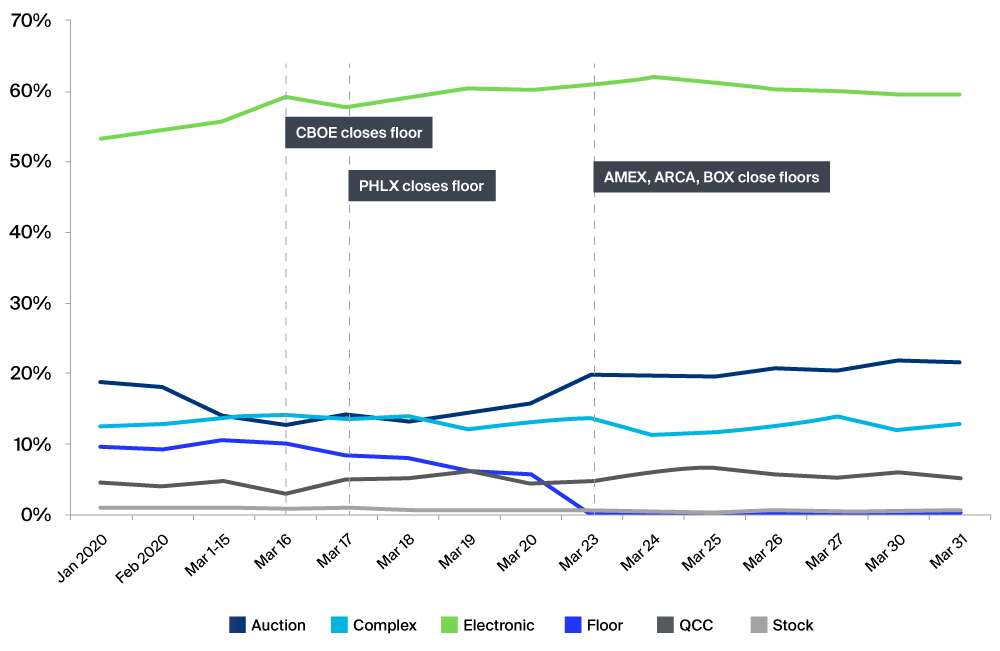

Social distancing measures in response to COVID-19 forced options trading floors to temporarily suspend operations. CBOE closed their options trading floor on March 16, followed by PHLX on March 17, and NYSE American, NYSE ARCA, and BOX on March 23.

- Following the temporary closures of all options trading floors, options industry average daily contracts dropped from 28.5 million in the first 3 weeks to 23.3 million in the final week of March.

- About 5 million average daily contracts appear to be “missing” from industry volume, which may be floor volume that has not yet found an alternative way into the market or dispersion of trade desk personnel leading to decreased high-touch volume.

- Some floor volume may have been diverted to electronic auction mechanisms, as electronic auction share increased by about 6% in the final week of March after all floors were closed.

Trade Type Mix with Floor Closures

| March 1-15 | March 20 | March 31 | |

| Electronic | 55.8% | 60.4% | 59.6% |

| Auction | 14.2% | 15.7% | 21.5% |

| Complex | 13.7% | 13.1% | 12.9% |

| Floor | 10.5% | 5.7% | 0.0% |

| QCC | 4.7% | 4.4% | 5.2% |

| Stock | 1.1% | 0.7% | 0.7% |

Market Quality

In March, the market experienced the most rapid bear market in history, triggering substantial volatility in both the options market and the underlying cash market. Historically, the speed at which volatility changes—the “volatility of volatility”—tends to have the largest effect on options market quality.

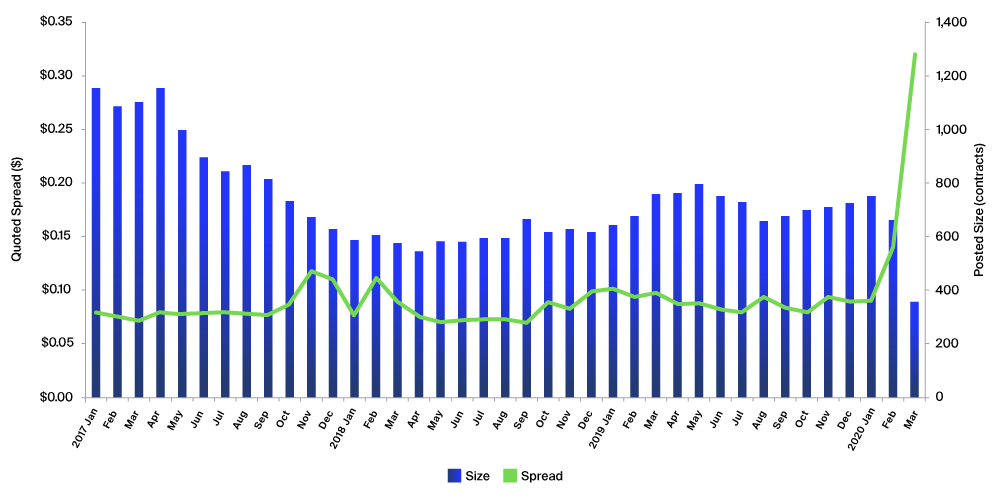

- From January to March, the average bid-ask spread width of options traded spiked from $0.09 to $0.32, a 256% increase.

- From January to March, average posted size declined 53%, dropping from 752 contracts per side in January to 354 contracts per side in March contracts.

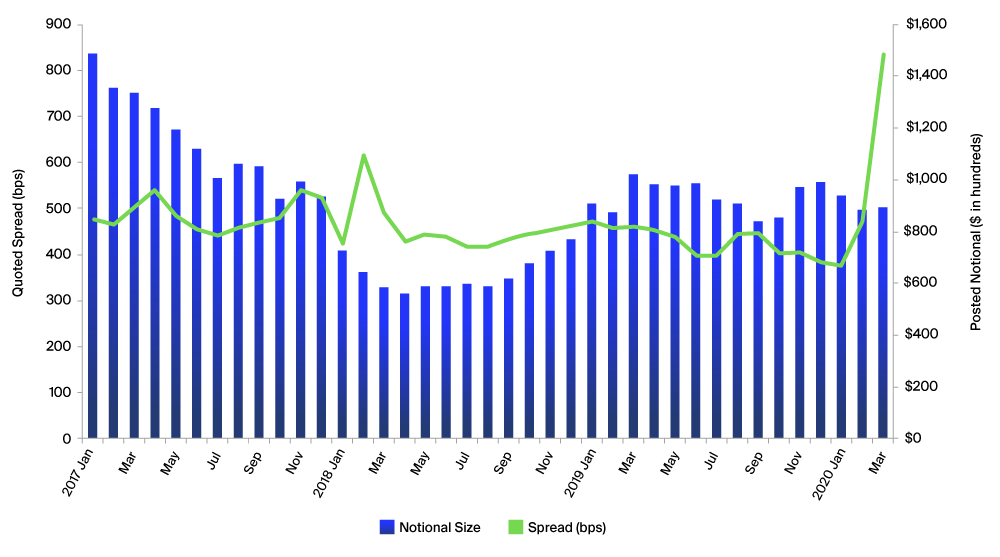

- Average spread width in basis points of option price increased 123% (374 bps to 835 bps) from January to March.

- Average posted notional size appeared relatively stable, down just 4.7% ($93,600 per side to $89,200) from January to March.

Quoted Spread ($) and Posted Size (contracts)

Quoted Spread (bps) and Posted Notional Size

Complexion Matters

While it is somewhat surprising that average posted notional size remained relatively stable while quoted contract size declined, this trend serves as a reminder that, when analyzing these averages over time, the moneyness and maturity of options traded should be considered in addition to implied volatility.

- Average price of options traded increased 86% from $2.91 in January to $5.41 in March.

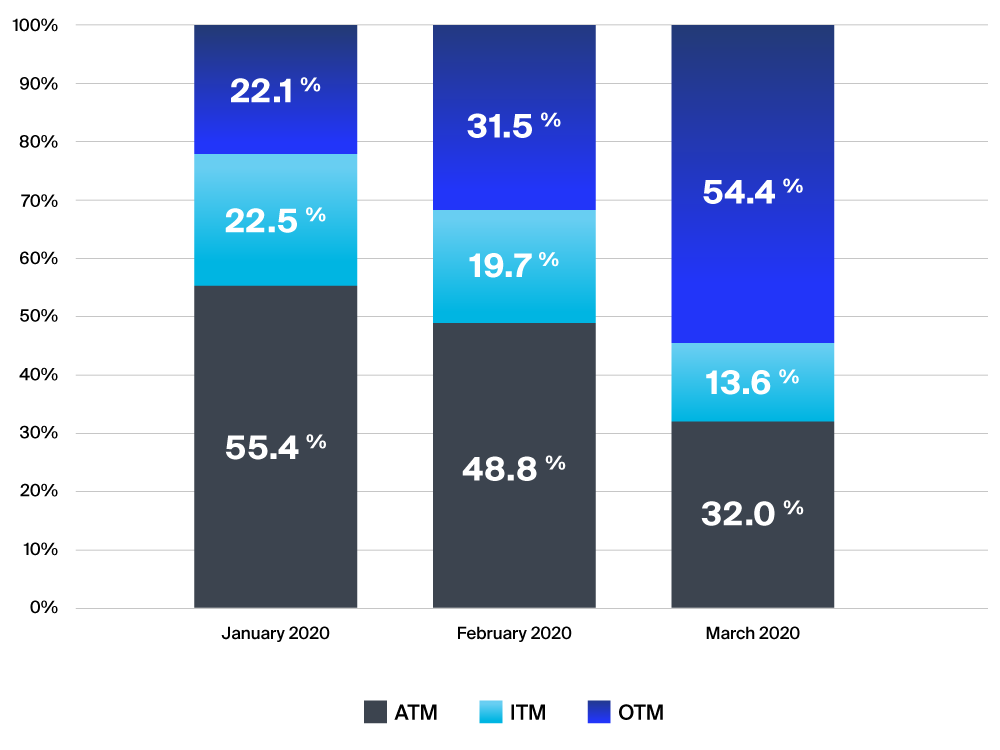

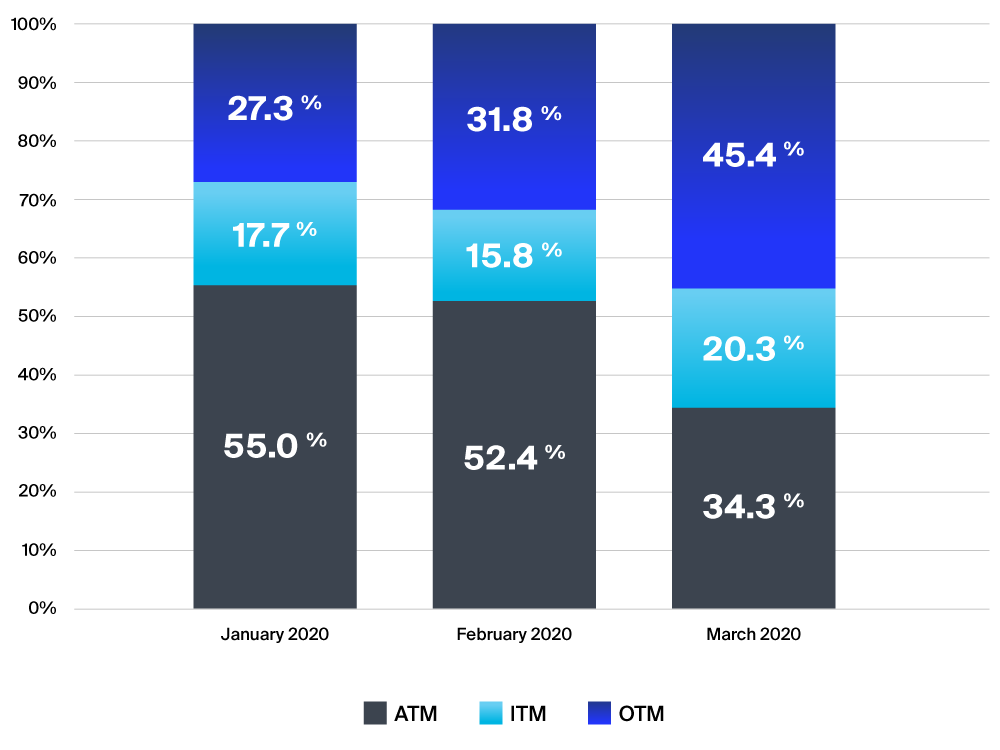

- There were dramatic shifts in the moneyness of options being traded with majority of trades shifting from at-the-money (ATM) options to out-of-the-money (OTM) options.

- ATM options comprised about 54% of options volume in the first half of the quarter and dropped to about 36% of volume in the second half.

- OTM options became more active series in the second half of the quarter as share of volume increased from 26% to 48%.

- ITM put options traded at a higher proportion than normal for two weeks in March, during some intense market sell-offs into new lows.

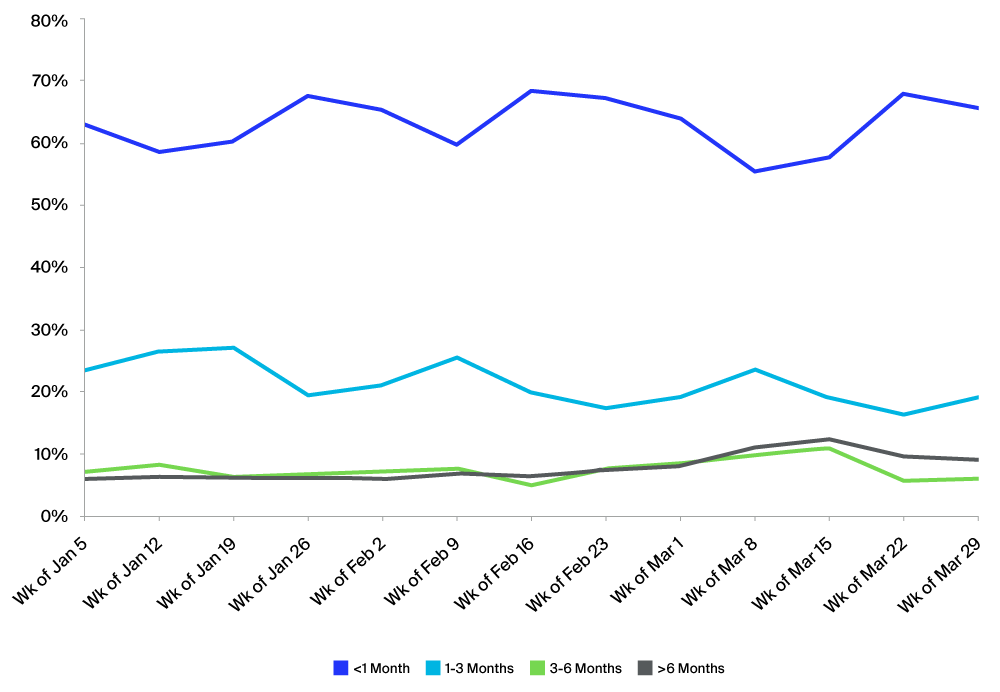

- Between January and March, there were also subtle shifts in options term maturity traded volumes, which are often hard to observe as front month options remained active due to the present day realized volatility.

- In the back months, volumes shifted from maturities of 1-3 months to 3-6 months and greater than 6 months as the uncertainty surrounding the duration and effects of the pandemic were expressed in the market. Notably, the longest dated options (>6 months maturity) overtook options in the 3-6 month expiration range in traded volume.

Call Moneyness

Put Moneyness

Options Maturity

Conclusion

Q1 2020 saw extraordinary options market volume and the unprecedented temporary closure of options trading floors. Beyond the volume and volatility numbers, there were several market microstructure shifts that could impact execution performance. Importantly, market participants should monitor trends such as the quoted size in notional terms and the moneyness and term maturity of options traded.

NYSE Research Insights

Find all of NYSE Research's articles on market quality, market structure, auctions, and options.