October 1, 2018

New Closing Price Logic

The price of a closing auction on the primary listing exchange determines the official closing price for most liquid corporate stocks and exchange-traded products (ETPs). However, many less-liquid securities do not receive sufficient closing-price interest to generate an auction. In such cases, the official closing price is based on the consolidated last sale price before the end of trading. This presents a distinct problem for less-liquid ETPs: if the underlying index/underlying fund holdings and corresponding market maker quotes have changed, but there have not been any consolidated last sales in the closing minutes of the market, the consolidated last sale value will not reflect current market pricing. This will then cause a greater disparity between the market price and its underlying net asset value (NAV). Around two-thirds of listed ETPs fit into this category.

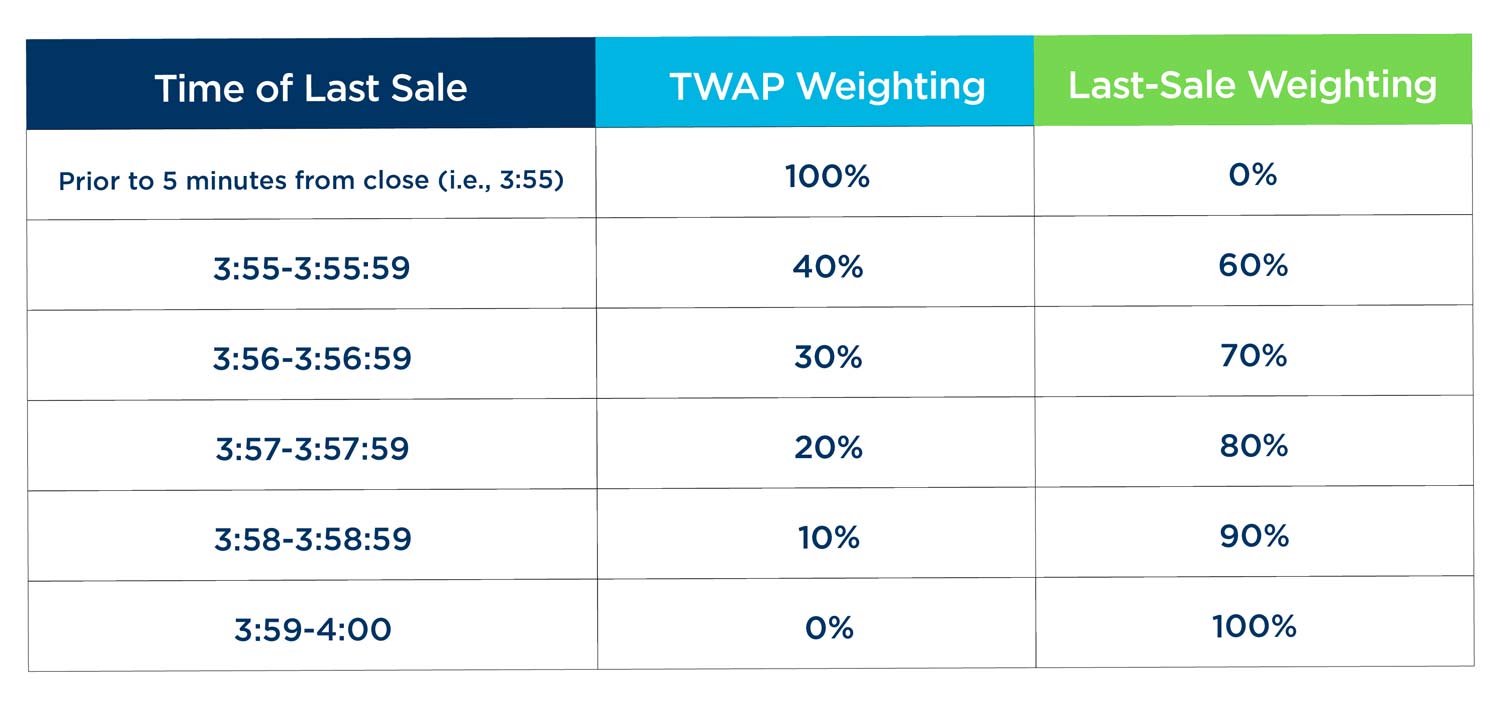

To address this issue, in June, NYSE Arca introduced a process for setting an official closing price for its listed ETPs that better reflects the true value for ETPs that do not end trading with a closing auction. The new Arca Official Closing Price (AOCP) methodology for NYSE Arca-listed ETPs applies when an ETP does not have a closing auction, or the closing auction is an odd lot. Previously, the AOCP for ETPs without an eligible closing auction was the consolidated last sale, regardless of when the last sale occurred - be that days, weeks or even months prior.

The new AOCP methodology uses both consolidated last sale and National Best Bid and Offer (NBBO) inputs. NYSE Arca tracks the time-weighted average midpoint price (TWAP) of the NBBO over the last five minutes of the trading day. The TWAP and the consolidated last sale are blended based on the last sale time to determine the AOCP, according to the following schedule:

AOCPs derived solely from quoting activity account for 44% of total closing prices, while AOCPs reflecting a mix of trade and quote activity account for 5% of the total.

Performance Assessment

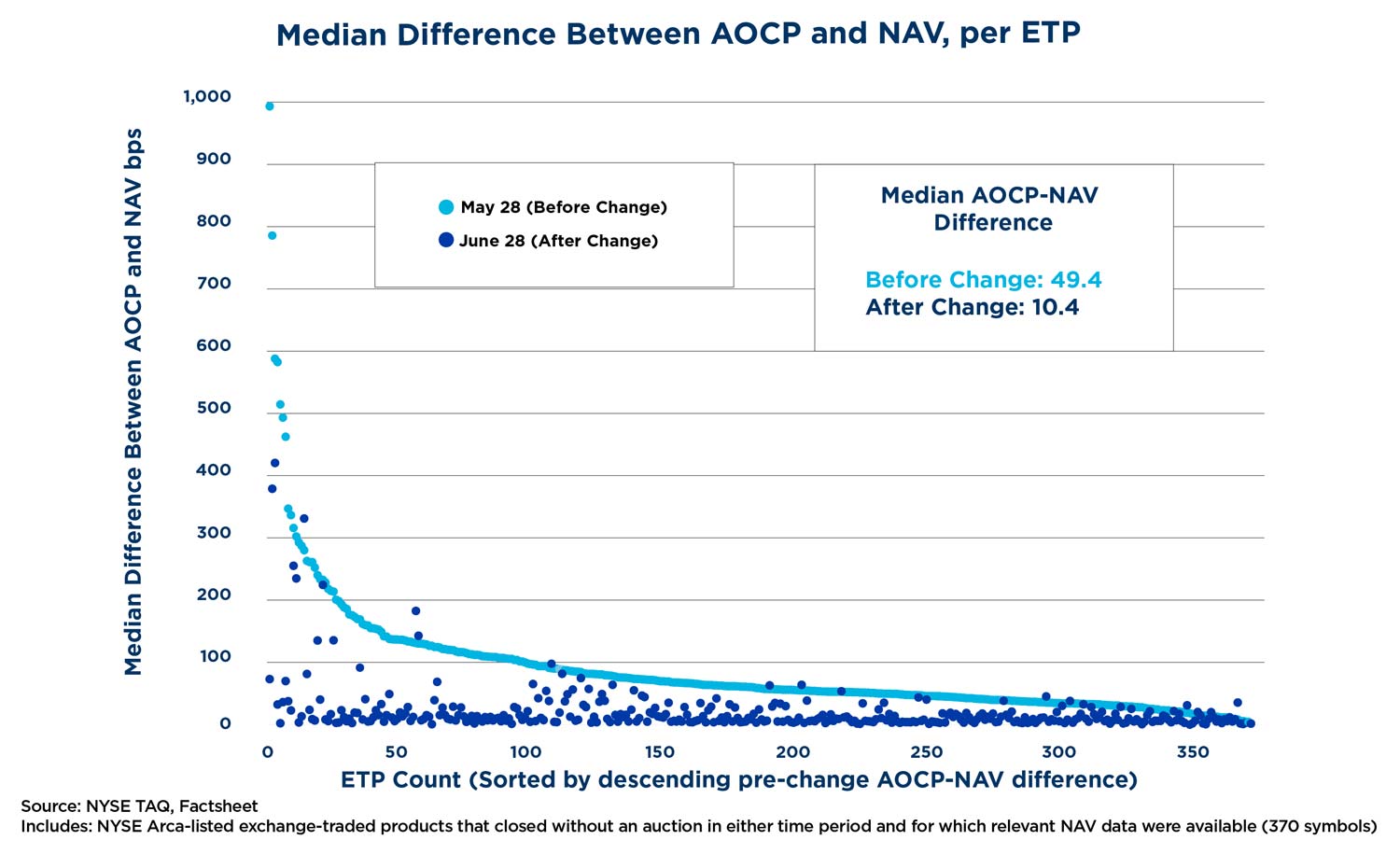

To assess the new logic's performance, we compared the difference between the AOCP and NAV Price before the logic took effect (May 1st 2018 - June 1st 2018) and after the logic was implemented (June 4th 2018 - June 30th 2018). We measured the average difference between the AOCP and NAV Price (at close) by product for each time period for products without auctions and then compared them across the before and after periods. As expected, the average difference between the AOCP and NAV tightened dramatically with the new logic.

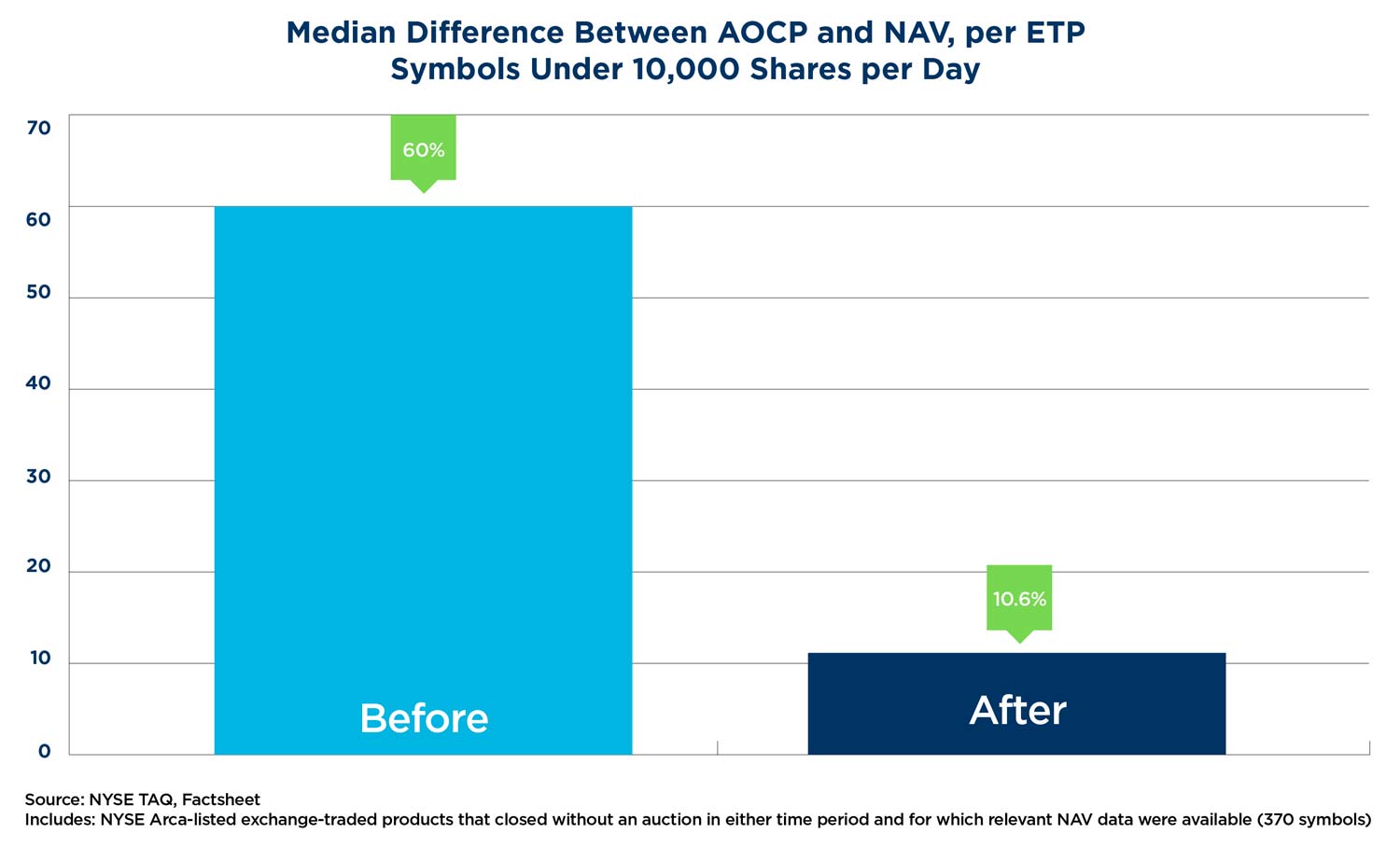

As expected, this performance improvement relative to NAV is most pronounced in the least-active products. For ETPs trading under 10,000 shares per day, the median difference between the AOCP and NAV decreased from 60 basis points previously to 10.6 basis points using the new logic. Because the AOCP sets the reference price for the 'Limit Up Limit Down' (LULD) mechanism on the next trading day, an AOCP more closely aligned with the NAV will reduce the potential for an LULD trading pause to be triggered. LULD is invoked during times of volatility and sets a percentage level above and below which a security can move within a five-minute period. A security is automatically halted if the price would move outside the set percentage levels. An incorrect reference price is likely to lead to more LULD trading pauses because it does not reflect the value of the security.

Summary

As these results demonstrate, the new AOCP logic produces closing prices closer to NAV for the nearly two-thirds of ETPs that close without an auction each day. In addition to helping fix hard-to-explain premiums/discounts due to stale data, a more accurate official closing price also helps provide market protection with better reference prices to LULD. Furthermore, since ETPs report market price returns versus returns on NAV, stale closing prices can inaccurately skew performance data. This is of particular concern on month-end, quarter-end, and year-end dates.

NYSE Research Insights

Find all of NYSE Research's articles on market quality, market structure, auctions, and options.