December 5, 2019

An options trade periodically seen in the options market is the Dividend Spread. A dividend spread trade involves simultaneously buying calls at one strike price while selling calls at a different strike price, in which both calls are optimal to exercise (in-exercise) before a stock’s ex-dividend (ex-div) date. Traders engaging in this trade exercise their long calls from the trade, which creates a position of being long stock against their short calls from the spread. The traders using this strategy may profit from being short the in-exercise calls, if the holders of the long call positions do not exercise. On the ex-div date, if the traders are assigned on less than their full short call position, they may profit as the calls lose value when the share price falls, while their loss in the long stock position is exactly offset by the receipt of the dividend.

These trades are clustered before a stock’s ex-div date and tend to occur in such great volume that they distort market volume and exchange market share statistics for those trading days. For example, when AAPL and nearly 80 other stocks recently went ex-div, average daily volume (ADV) in the securities increased by 236% compared to their year-to-date ADVs.

In December 2012, the Securities Industry and Financial Markets Association (SIFMA) asked the Options Clearing Corporation (OCC) to formally review the Dividend Spread strategy. After completing its review, the OCC filed a rule change with the SEC that it believed would significantly restrict the strategy. In this filing, the OCC noted that the industry may negatively view dividend plays, and that the trades are unfair to retail investors and distortive to options transactions volume.

PHLX and BOX are the only two options exchanges (out of 16) that treat dividend strategies as a “capped strategy trade” eligible for reduced fees. In the absence of the cap, the trade would likely be more cost prohibitive on a per contract basis due to the large volumes being traded. BOX only just recently filed to incentivize this strategy in May.

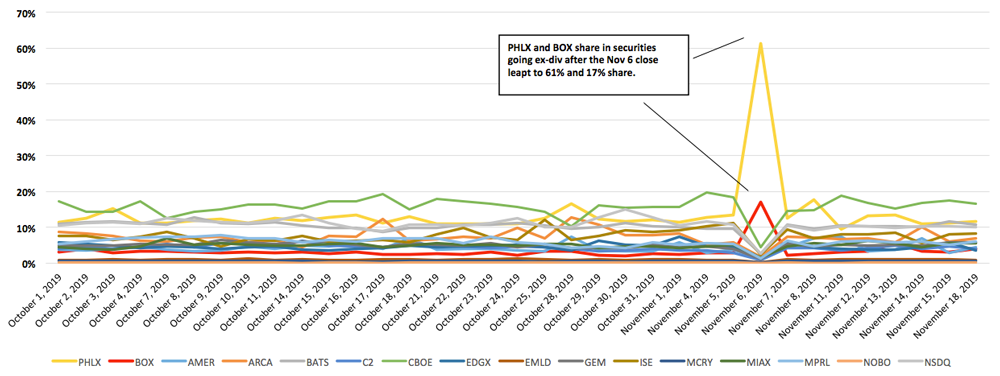

This pricing structure has dramatic market share impact. For example, in the securities that went ex-div after the close on November 6, 2019, PHLX increased its market share in these securities to 61.4% from 15.2%, and BOX increased to 17% from 3.5%.

Exchange Market Share in Ex-Div Symbols

These market share blips should be understood for what they are - exchanges providing financial incentives for otherwise cost-prohibitive trading strategies. These market share distortions bear no relation to any other changes to the underlying security that could otherwise result in increased trading activity in an options issue.

The Dividend Spread Trade

To illustrate how Dividend Spread trades are costly in the absence of any fee incentives, it is helpful to understand the mechanics of how these trades work.

1. Early Exercise of Call Options

Only shareholders of dividend-paying stocks are entitled to receive the dividend. On the ex-div date, a stock’s share price trades minus the amount of the dividend. Owners of call options are not entitled to receive any dividends, and the calls lose value corresponding to the decline in the share price after the stock trades ex-div. This makes it potentially optimal to exercise a call on the day before the ex-div date.

It is optimal to early exercise a call before the ex-div date if the present value of the dividend less the cost to carry the stock is greater than the remaining time value of the option, which can be represented by the value of the put. This typically means that deep in-the-money calls with little to no remaining time value are “in-exercise.”

2. Putting on the Trade

Before a stock’s ex-div date, options traders engaging in dividend spread trades seek out call options that are in-exercise and have large open interest. Deep in-the-money calls that are in-exercise are usually 100 delta or very close, so a dividend spread that involves buying one of these calls and selling another deep call at a different strike price is a delta neutral trade. These spreads trade at parity in large volumes, usually multiples more than the open interest.

When options are exercised, options assignments are allocated among the short interest pool by the OCC. The OCC document on Assignment Procedure can be found here. Traders that traded dividend spreads exercise all of the calls that they purchased that day and receive stock. Their hope is that OCC assignments do not call away their long stock, which could happen if anyone who is long the calls failed to exercise against the traders’ short call positions. Traders that are not assigned on the short call/long stock position receive the dividend on their long stock, while remaining short on the calls.

Without the “capped strategy trade” treatment for dividend spreads on PHLX and BOX, normal fees would apply on a per contract basis. Typically, only a small percentage of in-exercise calls go un-exercised, and traders would need a much higher percentage to offset normal transaction fees on a two-legged dividend spread.

3. Simplified Example

The following example is fictional and for illustrative purposes only:

- Assume Trader A buys 10,000 contracts of a parity call spread from Trader B, an amount which dwarfs the previous open interest in both call strikes, the day before the stock trades ex-div.

- When the market closes, both Traders A and B exercise their long calls from the call spread.

- Now only short the call sales from the call spreads (and long stock from the exercised calls), the traders hope that the OCC assignment process results in them receiving assignments on less than their entire positions.

- If this happens, they will remain short some calls and long XYZ shares, on which they will receive the dividend.

- Remaining options exposure can be hedged by buying inexpensive puts to leg into the “conversion” side of a reversal/conversion trade.

- The large volume of the trade served to crowd out the original natural short call open interest and effectively transferred most of the profitable short call, long stock position to the two traders.

NYSE Research Insights

Find all of NYSE Research's articles on market quality, market structure, auctions, and options.