January 18, 2019

Volatility returned to US markets in 2018, leading to record equity options trading volumes. At the same time, there was increased interest in options market quality, particularly as it relates to the displayed quote.1 Given NYSE’s advocacy for robust displayed markets, and the unique nature of the year’s volatility and volume, 2018 was an ideal year to study the influence of volatility on quoted spread and size. We found that adjustments for option prices can dramatically alter the interpretation of market quality metrics: after converting quoted bid-ask spread values from cents to basis points and converting quoted size from contracts to dollars, the data shows that displayed market quality was fairly consistent during some of 2018’s volatile periods.

Methodology

Our analysis leveraged NBBO quote data provided from S3 and was limited to the top 15% of symbols by options ADV. We focused on options with underlying symbols that had at least 1,000,000 shares of ADV, removed any new listing and delisting, and removed symbols that changed Penny Pilot groups during the year. Finally, we excluded SPY so as to not skew the results. SPY accounts for nearly 20% of options volume, and this scale likely gives it market structure attributes not common to the rest of the tradable universe. The resulting list of symbols accounted for 71% of total equity options volume.

We calculated our normalized spread as a percent of average option price in basis points:

NBBO Spread (% bps) = Avg NBBO Spread Width ($) / Avg Option Trade Price ($)

Size was converted from contracts to dollars by calculating notional size:

NBBO Notional Size ($) = Avg NBBO Size × Avg Option Trade Price

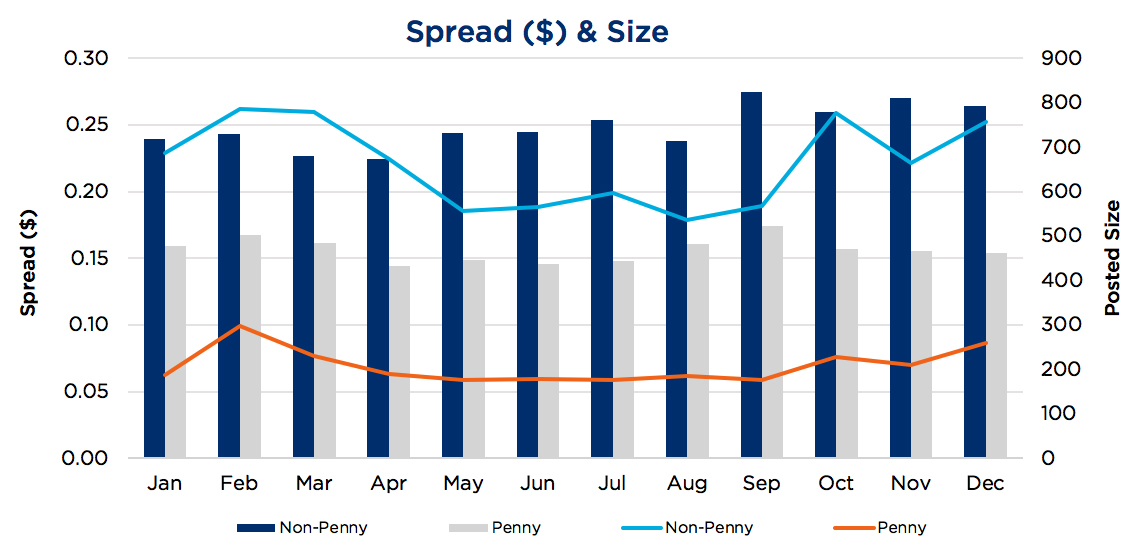

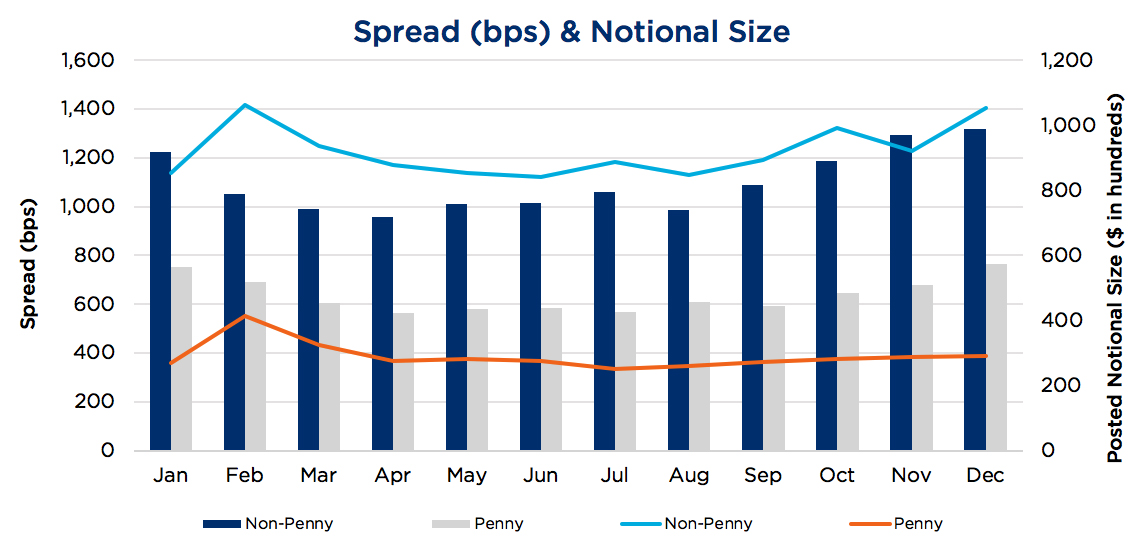

Penny vs Non-Penny Spread and Size Comparison

In the charts below, we plotted monthly average spread and size for Penny Pilot (PP) and Non-Penny Pilot (NPP) symbols. In 2018, NPP names had a spread of roughly 3x the spread of PP names, accompanied by 60% greater size compared to PP names. NPP posted size fluctuated over the year, ending the year higher than it began. We also observed that spread widths for NPP symbols fluctuated more than PP symbols in nominal terms, but less so using normalized measures.

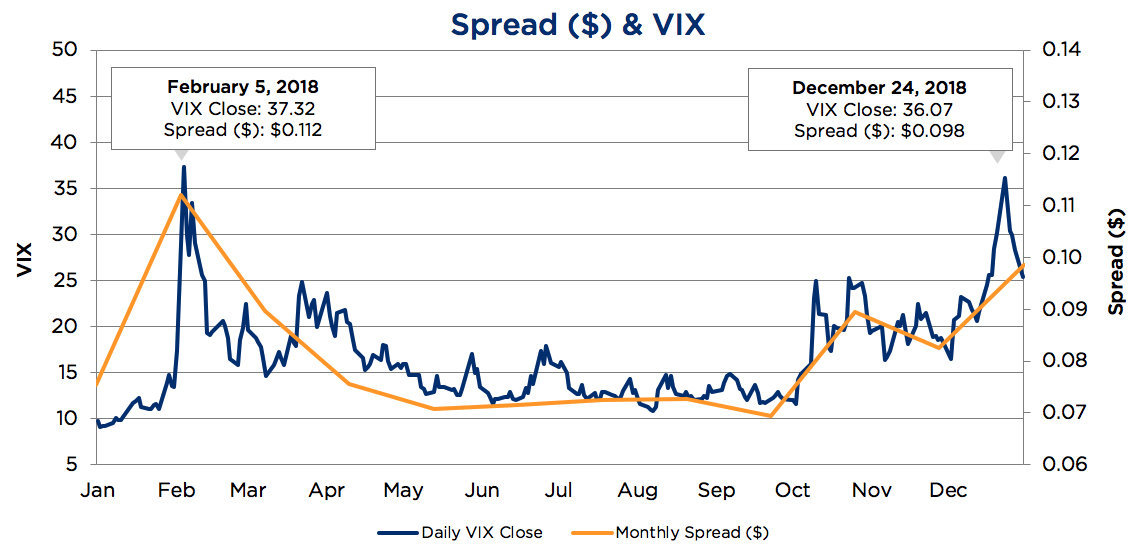

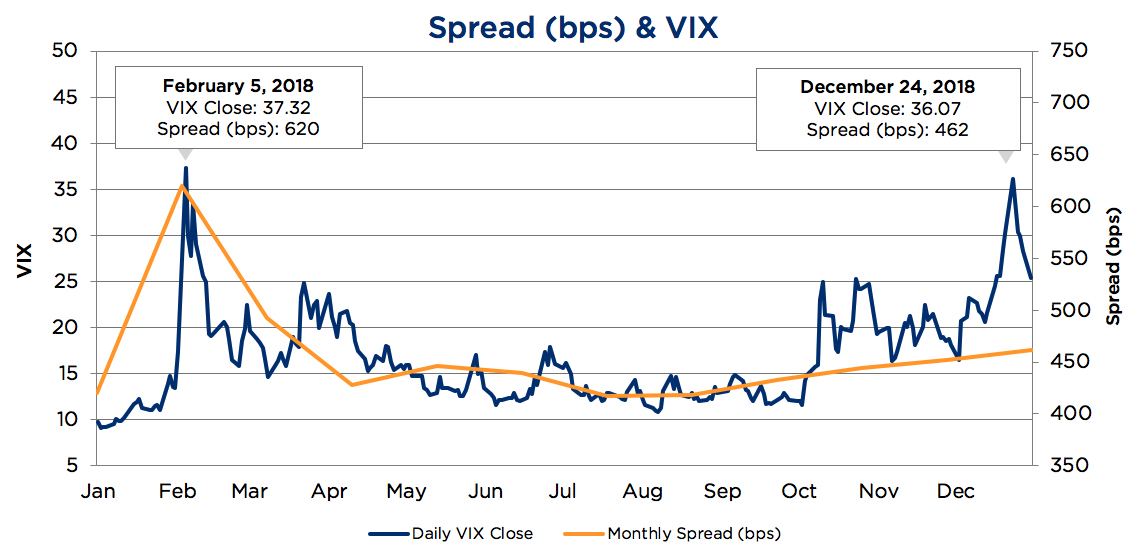

How Did Volatility Affect Option Spreads?

Nominal spreads followed the fluctuations of the VIX closely. We saw nominal spreads widen with the elevated VIX levels in February and March, as well as in October through the end of the year. When we adjust the spread calculation to show percent of option price in basis points, spreads still appeared wider in February, but were more muted the rest of the year. We hypothesize that the speed at which VIX spiked in February, moving from 13.47 to 37.32 in two trading days, had a greater impact on spread widths compared to the more gradual rise of VIX across months late in the year when it rose from 11.61 to 36.07 in 56 trading days. The normalization shows that although nominal spreads increased, they increased proportionally and in tandem with option prices. In our population, average option prices increased by 31.5%, whereas spread widths only increased by 25.5% in Q4.

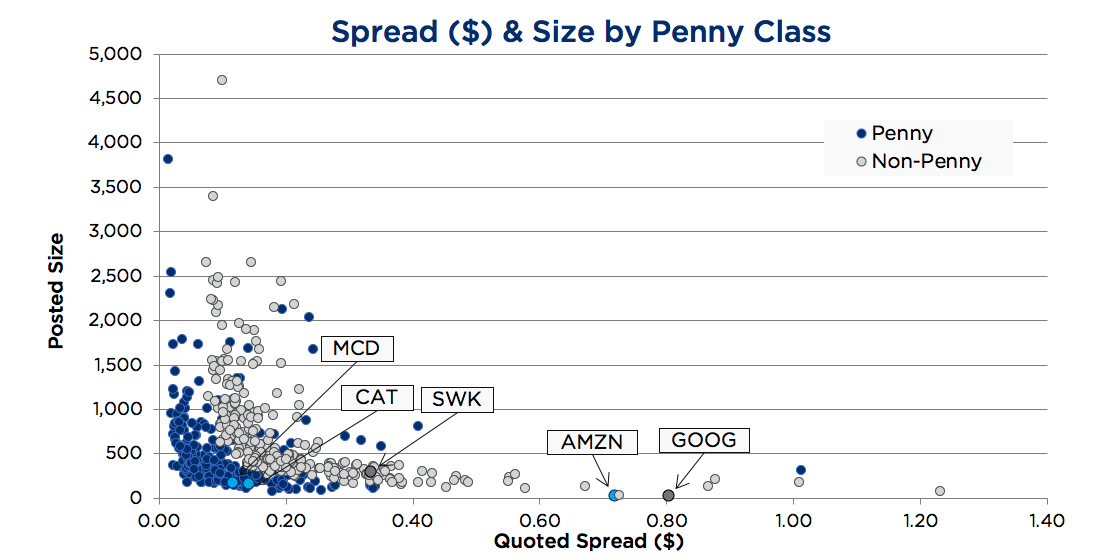

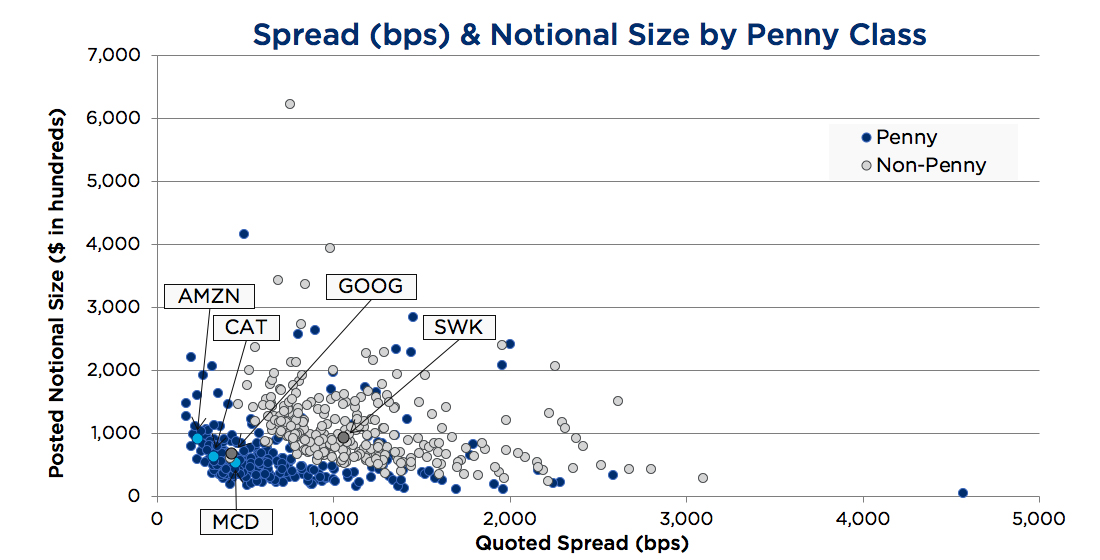

Spread and Size of Individual Symbols

The impact of these price normalization steps can be particularly meaningful at an individual symbol level. In nominal terms, high-priced symbols Google (GOOG) and Amazon (AMZN) had some of the worst spreads and posted size. However, in notional terms, GOOG had the tightest quoted spread of all non-penny symbols (422 bps) and moved much closer to the average posted notional size of $85,000; AMZN experienced similar results. Additionally, household names such as McDonald’s (MCD), Caterpillar (CAT), and Stanley Black & Decker (SWK) exhibited tightened quoted spreads after we converted from nominal terms to basis points. We believe that converting spread and size to notional terms may change perceptions of market quality and improve the ability to compare among symbols.

Summary

Unlike the US listed options market, many global markets of various asset classes use notional values for quote and trade increments. The above analysis details the merit of using notional values for assessing US listed options market quality, especially in highly volatile times. This perspective shows that the US listed options market handled 2018’s volatility fairly well, particularly when the elevated volatility was sustained over a period of time.

1 Pensions & Investments: Exchange, industry group petitions SEC to create committee on options market

NYSE Research Insights

Find all of NYSE Research's articles on market quality, market structure, auctions, and options.