August 13, 2020

Ed Rosenberg

Head of ETFs, American Century

American Century has a long-standing track record as an active asset manager. What led to the decision to enter the active ETF market in late 2019?

American Century has a long history in the active management space, and launching active ETFs was a natural extension of what we do well. Launching strategies in the ETF wrapper originated from client requests. It was our response to client demand while also introducing actively managed solutions that have been part of American Century’s DNA for more than 60 years.

American Century has experienced early success in the market, recently eclipsing $1 billion in YTD cash flow and over $2 billon in AUM. What activities do you attribute this success to?

Our objective was to launch ETFs that resonate with clients. We took the time to listen to what our clients were looking for and embraced an approach that allowed us to introduce products where they had an interest in investing. We began with transparent products while waiting for one or more of the semi-transparent structures to be approved by the SEC. Our sales team has played a critical role in selling our ETFs because they have embraced the various structures and can customize solutions to the clients’ needs.

American Century is unique in offering active ETFs with various levels of transparency. What led to the decision to offer multiple structures and license from ActiveShares and the NYSE?

When we first started looking at the different structures back in 2017, it was difficult to predict client preferences and if they would favor one structure over another. We also thought there were some really good structures that would get approved and have longevity. Considering those two factors drove the decision to license more than one structure. We believe they both have positives that make sense for our ETFs and are extremely happy to be the first to launch in both the Precidian ActiveShares and NYSE proxy basket structure. In just two and half years, we have built one of the most diverse ETF platforms in the history of our industry. Our line-up includes rules-based index ETFs, active, both transparent and in two different semi-transparent structures. There is no platform today with this type of varied offerings.

What are your early observations on the trading and adoption of American Century’s four semi-transparent ETFs? What hurdles do you see on the horizon?

The semi-transparent ETFs have been extremely well received by the ecosystem and clients. Our lead market maker, Citadel, has done an exceptional job keeping spreads consistent since the day we launched our first semi-transparent product, which just happened to be in the middle of one of the worst market downturns in history. Client demand has been exceptional. Clients have approached us about our products whom we have never done business with before. Across all four semi-transparent ETFs, we are approaching $300M since March 31.

As for the biggest hurdle, it is the same with any new ETF, platform availability. They are currently on the RIA and retail platforms. The hope is that we will expand beyond that in the near future.

What guidance would you provide sponsors as they consider expanding their product offer to include actively managed ETFs (either fully transparent or semi-transparent)?

If you are a new firm looking to launch ETFs for the first time, make sure you bring on someone or a team with experience. The ETF Capital Markets function is often overlooked and it is one of the most important functions to have as you enter the ETF marketplace.

Really understand the ETF ecosystem because every choice you make is important; from your custodian and their ability to handle ETFs, to a distributor, to a lead market maker, and the exchange. Really understanding the capabilities of each and how they can help you launch an ETF and become successful is extremely important. As an example, we have found our partnership with the NYSE to be extremely beneficial when we went into the ETF business.

The last thing I would say is you need a strong sales plan. ETFs are sold and not bought. It is exceptionally important to have the right sales team in place, whether that is an existing one or a new one, to really push the ETF from the moment it starts trading.

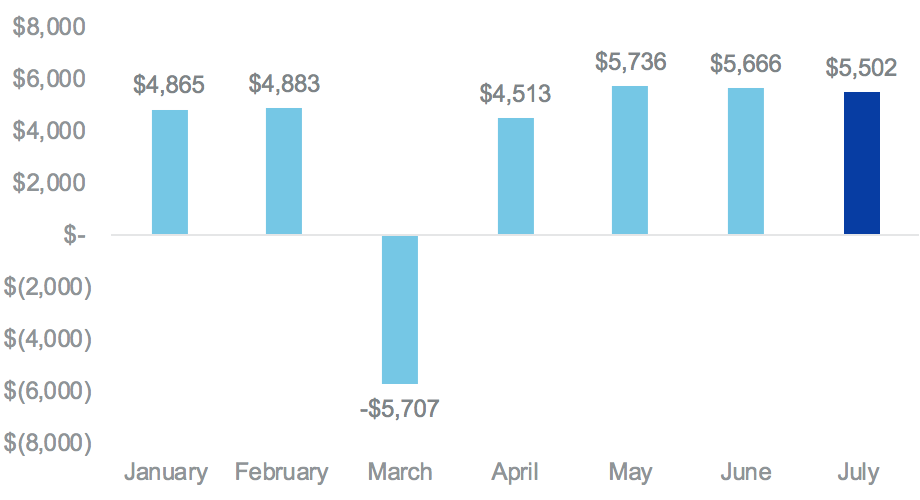

Active ETF momentum carries through July

The active ETF market's momentum didn't fade in July. Cash flow was shy of record levels, but rising markets combined with $5.5 billion in new cash flow elevated assets to a record high of $128 billion

Active ETF Cash Flow

Source: Factset as of 7/31/2020

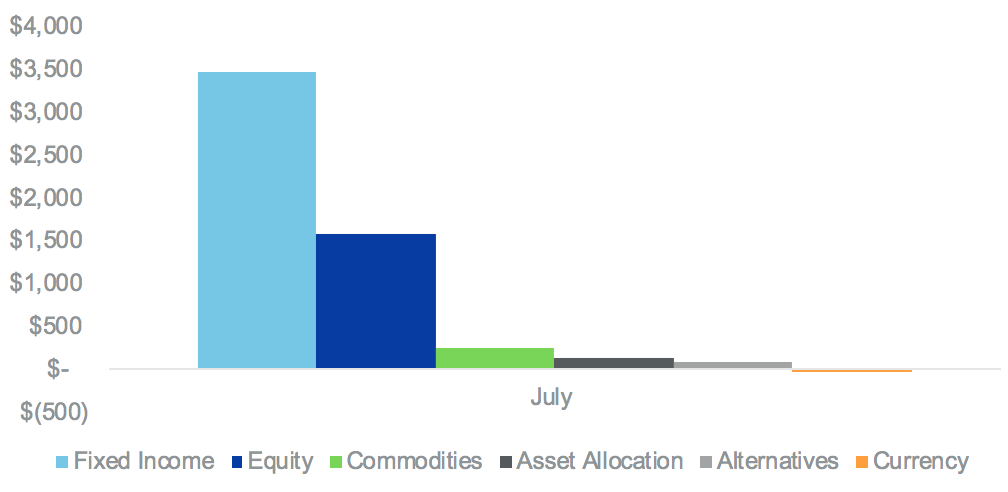

During July, fixed income products led the industry in cash flow with $3.5 billion supported by investor interest in short and ultra-short-term investment grade credit ETFs from J.P. Morgan, Invesco, iShares and Janus Henderson. Equity cash flow set a new high for the year at $1.6 billion led by ARK's suite of innovation-focused ETFs.

July Active ETF Cash Flow by Asset Category

Source: Factset as of 7/31/2020

Top 5 Issuers by Cash Flow

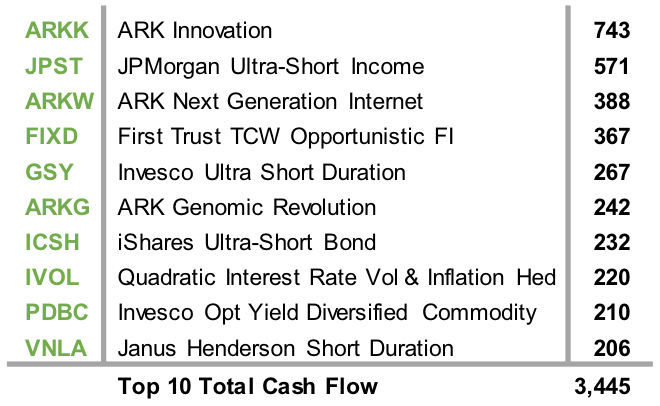

Top 10 ETFs by Cash Flow ($M)

Source: Factset as of 7/31/2020

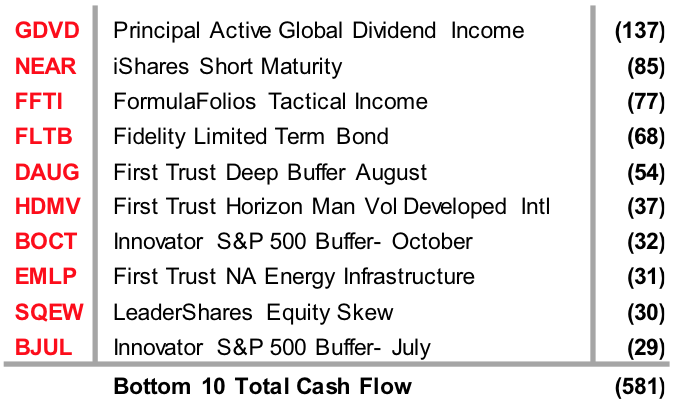

Bottom 10 ETFs by Cash Flow ($M)

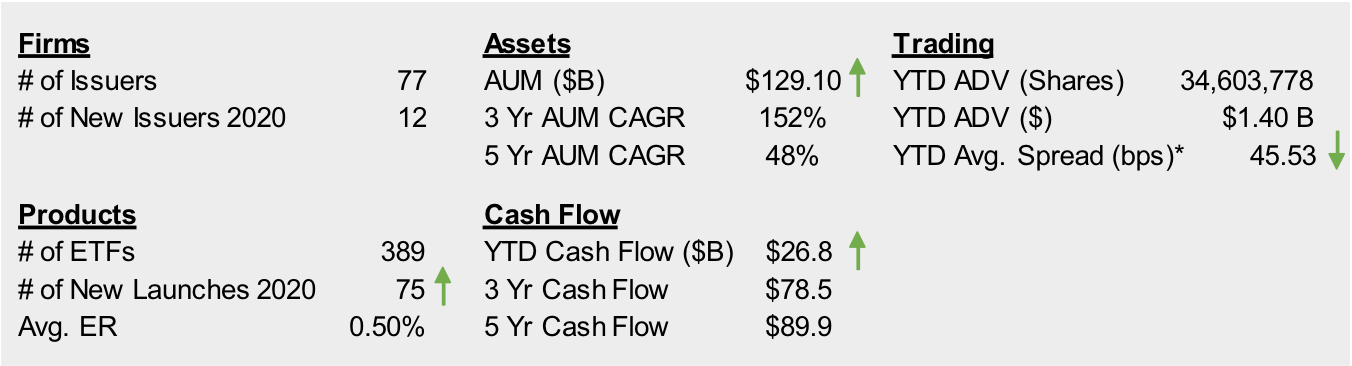

ETF Stat Pack

Source: Factset & NYSE Internal Database and Consolidated Tape Statistics as of 8/7/2020

*Simple average